导入计算库

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

plt.style.use("fivethirtyeight")

plt.rcParams["font.sans-serif"] = ["Microsoft YaHei"]

plt.rcParams["axes.unicode_minus"] = False

from sklearn.preprocessing import OneHotEncoder

import statsmodels.api as sm

from statsmodels.graphics.tsaplots import plot_acf,plot_pacf

from pandas.tseries.offsets import DateOffset

from statsmodels.tsa.arima.model import ARIMA

import warnings

warnings.filterwarnings("ignore")

导入数据

path_train = "../preocess_data/train_data_o.csv"

path_test = "../data/test_data.csv"

data = pd.read_csv(path_train)

data_test = pd.read_csv(path_test)

data["运营日期"] = pd.to_datetime(data["运营日期"] )

data_test["运营日期"] = pd.to_datetime(data_test["日期"])

data.drop(["行ID","日期"],axis=1,inplace=True)

data_test.drop(["行ID","日期"],axis=1,inplace=True)

折扣编码

enc = OneHotEncoder(drop="if_binary")

enc.fit(data["折扣"].values.reshape(-1,1))

enc.transform(data["折扣"].values.reshape(-1,1)).toarray()

enc.transform(data_test["折扣"].values.reshape(-1,1)).toarray()

array([[0.],

[0.],

[0.],

...,

[1.],

[0.],

[0.]])

data["折扣"] = enc.transform(data["折扣"].values.reshape(-1,1)).toarray()

data_test["折扣"] = enc.transform(data_test["折扣"].values.reshape(-1,1)).toarray()

日期衍生

def time_derivation(t,col="运营日期"):

t["year"] = t[col].dt.year

t["month"] = t[col].dt.month

t["day"] = t[col].dt.day

t["quarter"] = t[col].dt.quarter

t["weekofyear"] = t[col].dt.weekofyear

t["dayofweek"] = t[col].dt.dayofweek+1

t["weekend"] = (t["dayofweek"]>5).astype(int)

return t

data_train = time_derivation(data)

data_test_ = time_derivation(data_test)

对每家店进行探索

对第一家尝试

# 训练集合

data_train_1 = data_train[data_train["商店ID"] ==1]

# 测试集合

data_test_1 = data_test_[data_test_["商店ID"] ==1]

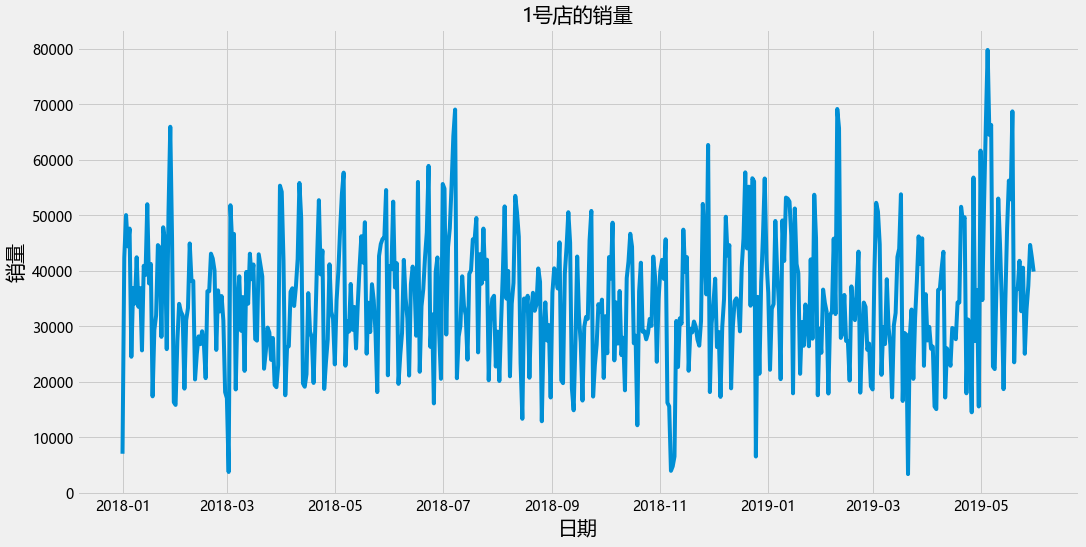

plt.figure(figsize=(16,8))

plt.plot(data_train_1["运营日期"],data_train_1["销量"])

plt.xlabel("日期",fontsize= 20)

plt.ylabel("销量",fontsize= 20)

plt.title("1号店的销量",fontsize=20)

Text(0.5, 1.0, '1号店的销量')

开始尝试

data_train_1.head()

| 商店ID | 商店类型 | 位置 | 地区 | 节假日 | 折扣 | 销量 | 运营日期 | year | month | day | quarter | weekofyear | dayofweek | weekend | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | S1 | L3 | R1 | 1 | 1.0 | 7011.84 | 2018-01-01 | 2018 | 1 | 1 | 1 | 1 | 1 | 0 |

| 607 | 1 | S1 | L3 | R1 | 0 | 1.0 | 42369.00 | 2018-01-02 | 2018 | 1 | 2 | 1 | 1 | 2 | 0 |

| 1046 | 1 | S1 | L3 | R1 | 0 | 1.0 | 50037.00 | 2018-01-03 | 2018 | 1 | 3 | 1 | 1 | 3 | 0 |

| 1207 | 1 | S1 | L3 | R1 | 0 | 1.0 | 44397.00 | 2018-01-04 | 2018 | 1 | 4 | 1 | 1 | 4 | 0 |

| 1752 | 1 | S1 | L3 | R1 | 0 | 1.0 | 47604.00 | 2018-01-05 | 2018 | 1 | 5 | 1 | 1 | 5 | 0 |

复制获得数据

data_train__1 = data_train_1.copy()

data_test__1 = data_test_1.copy()

删除不变的属性

data_train__1.drop(["商店类型","商店ID","位置","地区","运营日期"],axis=1,inplace=True)

data_test__1.drop(["商店类型","商店ID","位置","地区","运营日期"],axis=1,inplace=True)

在这里留下一个思考的点, 其实节假日的附近几天的属性也会对预测结果产生一定影响。

data_train__1.shape

(516, 10)

data_train__1

| 节假日 | 折扣 | 销量 | year | month | day | quarter | weekofyear | dayofweek | weekend | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 1.0 | 7011.84 | 2018 | 1 | 1 | 1 | 1 | 1 | 0 |

| 607 | 0 | 1.0 | 42369.00 | 2018 | 1 | 2 | 1 | 1 | 2 | 0 |

| 1046 | 0 | 1.0 | 50037.00 | 2018 | 1 | 3 | 1 | 1 | 3 | 0 |

| 1207 | 0 | 1.0 | 44397.00 | 2018 | 1 | 4 | 1 | 1 | 4 | 0 |

| 1752 | 0 | 1.0 | 47604.00 | 2018 | 1 | 5 | 1 | 1 | 5 | 0 |

| … | … | … | … | … | … | … | … | … | … | … |

| 186569 | 0 | 1.0 | 33075.00 | 2019 | 5 | 27 | 2 | 22 | 1 | 0 |

| 187165 | 0 | 1.0 | 37317.00 | 2019 | 5 | 28 | 2 | 22 | 2 | 0 |

| 187391 | 0 | 1.0 | 44652.00 | 2019 | 5 | 29 | 2 | 22 | 3 | 0 |

| 187962 | 0 | 1.0 | 42387.00 | 2019 | 5 | 30 | 2 | 22 | 4 | 0 |

| 188113 | 1 | 1.0 | 39843.78 | 2019 | 5 | 31 | 2 | 22 | 5 | 0 |

516 rows × 10 columns

data_train__1["diff_1"] = data_train__1["销量"].diff(10)

data_train__1 = data_train__1.dropna()

# data_test__1["diff_1"] = data_test__1["销量"].diff(1)

# data_test__1 = data_test__1.dropna()

将数据集变为有监督数据集

def series_to_supervisied_(data,step_in,step_out,dropnan = True):

"""

:param data: 观测的序列,类型为列表或者二维的numpy数组

:param step_in: 作为输入滞后观测数量(x)

:param step_out: 作为输出的观测值数量(y)

:param dropnan: 是否具有Nan的行,默认为True

return 监督学习的重组得到的dataframe列

"""

n_vars = 1 if type(data) is list else data.shape[1]

df = data

cols = []

names = []

# 输入序列[(t-n),(t-n+1),(t-n+2)..(t-1)]

for i in range(step_in,0,-1):

cols.append(df.shift(i))

names+=[f"{name}-({i})step" for name in df.columns]

# 输出序列[t,(t+1),(t+2)...(t+n)]

for i in range(0,step_out):

cols.append(df.shift(-i))

if i ==0:

names+=[f"{name}+(0)step" for name in df.columns]

else:

names+=[f"{name}+({i})step" for name in df.columns]

df_re = pd.concat(cols,axis=1)

df_re.columns = names

if dropnan:

df_re.dropna(inplace=True)

return df_re

data_step = series_to_supervisied_(data_train__1,step_in= 10,step_out=2,dropnan = True)

data_step

| 节假日-(10)step | 折扣-(10)step | 销量-(10)step | year-(10)step | month-(10)step | day-(10)step | quarter-(10)step | weekofyear-(10)step | dayofweek-(10)step | weekend-(10)step | … | 折扣+(1)step | 销量+(1)step | year+(1)step | month+(1)step | day+(1)step | quarter+(1)step | weekofyear+(1)step | dayofweek+(1)step | weekend+(1)step | diff_1+(1)step | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 7658 | 0.0 | 0.0 | 36873.00 | 2018.0 | 1.0 | 11.0 | 1.0 | 2.0 | 4.0 | 0.0 | … | 0.0 | 44178.75 | 2018.0 | 1.0 | 22.0 | 1.0 | 4.0 | 1.0 | 0.0 | 18534.75 |

| 7791 | 0.0 | 0.0 | 25644.00 | 2018.0 | 1.0 | 12.0 | 1.0 | 2.0 | 5.0 | 0.0 | … | 0.0 | 28086.00 | 2018.0 | 1.0 | 23.0 | 1.0 | 4.0 | 2.0 | 0.0 | -12804.00 |

| 8337 | 0.0 | 1.0 | 40890.00 | 2018.0 | 1.0 | 13.0 | 1.0 | 2.0 | 6.0 | 1.0 | … | 0.0 | 47835.00 | 2018.0 | 1.0 | 24.0 | 1.0 | 4.0 | 3.0 | 0.0 | 8580.60 |

| 8610 | 1.0 | 1.0 | 39254.40 | 2018.0 | 1.0 | 14.0 | 1.0 | 2.0 | 7.0 | 1.0 | … | 1.0 | 45384.00 | 2018.0 | 1.0 | 25.0 | 1.0 | 4.0 | 4.0 | 0.0 | -6609.00 |

| 8821 | 0.0 | 1.0 | 51993.00 | 2018.0 | 1.0 | 15.0 | 1.0 | 3.0 | 1.0 | 0.0 | … | 1.0 | 25868.88 | 2018.0 | 1.0 | 26.0 | 1.0 | 4.0 | 5.0 | 0.0 | -11847.12 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 186152 | 0.0 | 1.0 | 47619.00 | 2019.0 | 5.0 | 16.0 | 2.0 | 20.0 | 4.0 | 0.0 | … | 1.0 | 33075.00 | 2019.0 | 5.0 | 27.0 | 2.0 | 22.0 | 1.0 | 0.0 | -23178.00 |

| 186569 | 0.0 | 1.0 | 56253.00 | 2019.0 | 5.0 | 17.0 | 2.0 | 20.0 | 5.0 | 0.0 | … | 1.0 | 37317.00 | 2019.0 | 5.0 | 28.0 | 2.0 | 22.0 | 2.0 | 0.0 | -15560.82 |

| 187165 | 1.0 | 1.0 | 52877.82 | 2019.0 | 5.0 | 18.0 | 2.0 | 20.0 | 6.0 | 1.0 | … | 1.0 | 44652.00 | 2019.0 | 5.0 | 29.0 | 2.0 | 22.0 | 3.0 | 0.0 | -24081.00 |

| 187391 | 0.0 | 1.0 | 68733.00 | 2019.0 | 5.0 | 19.0 | 2.0 | 20.0 | 7.0 | 1.0 | … | 1.0 | 42387.00 | 2019.0 | 5.0 | 30.0 | 2.0 | 22.0 | 4.0 | 0.0 | 18891.00 |

| 187962 | 0.0 | 0.0 | 23496.00 | 2019.0 | 5.0 | 20.0 | 2.0 | 21.0 | 1.0 | 0.0 | … | 1.0 | 39843.78 | 2019.0 | 5.0 | 31.0 | 2.0 | 22.0 | 5.0 | 0.0 | 3231.78 |

495 rows × 132 columns

list(data_step.columns)[-11:]

['节假日+(1)step',

'折扣+(1)step',

'销量+(1)step',

'year+(1)step',

'month+(1)step',

'day+(1)step',

'quarter+(1)step',

'weekofyear+(1)step',

'dayofweek+(1)step',

'weekend+(1)step',

'diff_1+(1)step']

y_columns = "销量+(1)step"

y = data_step[y_columns]

x = data_step[list(data_step.columns)[:-11]]

data_ = pd.concat([x,y],axis=1)

data_

| 节假日-(10)step | 折扣-(10)step | 销量-(10)step | year-(10)step | month-(10)step | day-(10)step | quarter-(10)step | weekofyear-(10)step | dayofweek-(10)step | weekend-(10)step | … | 销量+(0)step | year+(0)step | month+(0)step | day+(0)step | quarter+(0)step | weekofyear+(0)step | dayofweek+(0)step | weekend+(0)step | diff_1+(0)step | 销量+(1)step | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 7658 | 0.0 | 0.0 | 36873.00 | 2018.0 | 1.0 | 11.0 | 1.0 | 2.0 | 4.0 | 0.0 | … | 44625.00 | 2018 | 1 | 21 | 1 | 3 | 7 | 1 | 7752.00 | 44178.75 |

| 7791 | 0.0 | 0.0 | 25644.00 | 2018.0 | 1.0 | 12.0 | 1.0 | 2.0 | 5.0 | 0.0 | … | 44178.75 | 2018 | 1 | 22 | 1 | 4 | 1 | 0 | 18534.75 | 28086.00 |

| 8337 | 0.0 | 1.0 | 40890.00 | 2018.0 | 1.0 | 13.0 | 1.0 | 2.0 | 6.0 | 1.0 | … | 28086.00 | 2018 | 1 | 23 | 1 | 4 | 2 | 0 | -12804.00 | 47835.00 |

| 8610 | 1.0 | 1.0 | 39254.40 | 2018.0 | 1.0 | 14.0 | 1.0 | 2.0 | 7.0 | 1.0 | … | 47835.00 | 2018 | 1 | 24 | 1 | 4 | 3 | 0 | 8580.60 | 45384.00 |

| 8821 | 0.0 | 1.0 | 51993.00 | 2018.0 | 1.0 | 15.0 | 1.0 | 3.0 | 1.0 | 0.0 | … | 45384.00 | 2018 | 1 | 25 | 1 | 4 | 4 | 0 | -6609.00 | 25868.88 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 186152 | 0.0 | 1.0 | 47619.00 | 2019.0 | 5.0 | 16.0 | 2.0 | 20.0 | 4.0 | 0.0 | … | 25035.00 | 2019 | 5 | 26 | 2 | 21 | 7 | 1 | -22584.00 | 33075.00 |

| 186569 | 0.0 | 1.0 | 56253.00 | 2019.0 | 5.0 | 17.0 | 2.0 | 20.0 | 5.0 | 0.0 | … | 33075.00 | 2019 | 5 | 27 | 2 | 22 | 1 | 0 | -23178.00 | 37317.00 |

| 187165 | 1.0 | 1.0 | 52877.82 | 2019.0 | 5.0 | 18.0 | 2.0 | 20.0 | 6.0 | 1.0 | … | 37317.00 | 2019 | 5 | 28 | 2 | 22 | 2 | 0 | -15560.82 | 44652.00 |

| 187391 | 0.0 | 1.0 | 68733.00 | 2019.0 | 5.0 | 19.0 | 2.0 | 20.0 | 7.0 | 1.0 | … | 44652.00 | 2019 | 5 | 29 | 2 | 22 | 3 | 0 | -24081.00 | 42387.00 |

| 187962 | 0.0 | 0.0 | 23496.00 | 2019.0 | 5.0 | 20.0 | 2.0 | 21.0 | 1.0 | 0.0 | … | 42387.00 | 2019 | 5 | 30 | 2 | 22 | 4 | 0 | 18891.00 | 39843.78 |

495 rows × 122 columns

划分训练集测试集

lens = -1

from sklearn.model_selection import train_test_split

from sklearn.utils import shuffle

data_train_,data_test_ = train_test_split(data_,test_size=0.2,shuffle=False)

data_train_ = shuffle(data_train_,random_state=1412)

xtrain,ytrain = data_train_.iloc[:,:lens],data_train_.iloc[:,lens]

xtest,ytest = data_test_.iloc[:,:lens],data_test_.iloc[:,lens]

归一化

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

scaler.fit(ytrain.values.reshape(-1,1))

y_train = scaler.transform(ytrain.values.reshape(-1,1))

y_test = scaler.transform(ytest.values.reshape(-1,1))

随机森林

from sklearn.ensemble import RandomForestRegressor

rf_clf = RandomForestRegressor(max_depth=12,

min_impurity_decrease=0.0,

n_estimators= 300)

rf_clf.fit(xtrain,ytrain)

rf_clf.score(xtest,ytest)

0.43699715354836455

from sklearn.metrics import mean_squared_error

mean_squared_error(ytest,rf_clf.predict(xtest))**0.5

10330.02670862774

mean_squared_error(ytrain,rf_clf.predict(xtrain))**0.5

3440.408502696517

def symmetric_mean_absolute_percentage_error(y_true, y_pred):

y_true, y_pred = np.array(y_true), np.array(y_pred)

return np.sum(np.abs(y_true - y_pred) * 2) / np.sum(np.abs(y_true) + np.abs(y_pred))

def prophet_smape(y_true, y_pred):

smape_val = symmetric_mean_absolute_percentage_error(y_true, y_pred)

return 'SMAPE', smape_val, False

prophet_smape(ytrain,rf_clf.predict(xtrain))

('SMAPE', 0.07417421103653893, False)

prophet_smape(ytest,rf_clf.predict(xtest))

xgboost

from xgboost import XGBRegressor

xgb_clf = XGBRegressor(max_depth=12,

n_estimators=500)

xgb_clf.fit(xtrain,ytrain)

xgb_clf.score(xtest,ytest)

0.40055294233563

mean_squared_error(ytest,xgb_clf.predict(xtest))**0.5

10659.125252942618

mean_squared_error(ytrain,xgb_clf.predict(xtrain))**0.5

0.0036928046625203763

prophet_smape(ytest,xgb_clf.predict(xtest))

('SMAPE', 0.22077657322671448, False)

prophet_smape(ytrain,xgb_clf.predict(xtrain))

('SMAPE', 7.480844639369475e-08, False)

用一下贝叶斯优化看一下,是不是历史时间步长的问题?

from hyperopt import hp,fmin,tpe,Trials,partial

from hyperopt.early_stop import no_progress_loss

# 定义目标函数:

def hpyeropt_objective(params):

data_step = series_to_supervisied_(data_train__1,step_in = int(params["time_step"]),step_out=2,dropnan = True)

y_columns = "销量+(0)step"

y = data_step[y_columns]

x = data_step[list(data_step.columns)[:-20]]

data_ = pd.concat([x,y],axis=1)

from sklearn.model_selection import train_test_split

from sklearn.utils import shuffle

data_train,data_test = train_test_split(data_,test_size=0.2,shuffle=False)

data_train = shuffle(data_train,random_state=1412)

xtrain,ytrain = data_train.iloc[:,:-20],data_train.iloc[:,-1]

xtest,ytest = data_test.iloc[:,:-20],data_test.iloc[:,-1]

# 归一化

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

scaler.fit(ytrain.values.reshape(-1,1))

ytrain = scaler.transform(ytrain.values.reshape(-1,1))

ytest = scaler.transform(ytest.values.reshape(-1,1))

clf = RandomForestRegressor(n_estimators=int(params["n_estimators"]),

max_depth=int(params["max_depth"]),

# max_features=int(min(params["max_features"],len(xtrain.columns))),

min_impurity_decrease=params["min_impurity_decrease"],

random_state=1412,

verbose=False,

n_jobs=-1

).fit(xtrain,ytrain)

scores = clf.score(xtest,ytest)

return -scores

#定义参数空间

params_grid = {"n_estimators":hp.quniform("n_estimators",10,1000,20),

"max_depth":hp.quniform("max_depth",5,25,1),

# "max_features":hp.quniform("max_features",10,10000,1),

"min_impurity_decrease":hp.quniform("min_impurity_decrease",0,5,1),

"time_step":hp.quniform("time_step",10,200,5)

}

#定义迭代

def param_hyperopt(max_evals = 100):

trials = Trials()

early_stop_fn =no_progress_loss(50)

params_best = fmin(hpyeropt_objective,

space=params_grid,

algo=tpe.suggest,

max_evals=max_evals,

verbose=True,

trials=trials,

early_stop_fn=early_stop_fn

)

print("\n","\n","best params:",params_best,"\n")

return params_best,trials

params_best,trials = param_hyperopt(max_evals = 300)

34%|███████████████ | 103/300 [02:59<05:43, 1.75s/trial, best loss: -0.48958559215129405]

best params: {‘max_depth’: 9.0, ‘min_impurity_decrease’: 0.0, ‘n_estimators’: 660.0, ‘time_step’: 10.0}

目前来讲的话,效果都不是很好,那么接下来从时间角度来想的话,在每个时间窗内进行差分以及其他的特征衍生,尽量的提取一些其他的特征! 至此先考虑下另外一个方案。

data_train__1["销量"].diff()-data_train__1["销量"].diff()

| 节假日 | 折扣 | 销量 | year | month | day | quarter | weekofyear | dayofweek | weekend | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.0 | 0.0 | -35357.16 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 607 | 0.0 | 0.0 | -7668.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 1046 | 0.0 | 0.0 | 5640.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 1207 | 0.0 | 0.0 | -3207.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 1752 | 0.0 | 1.0 | 23109.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | -1.0 |

| … | … | … | … | … | … | … | … | … | … | … |

| 186569 | 0.0 | 0.0 | -4242.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 187165 | 0.0 | 0.0 | -7335.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 187391 | 0.0 | 0.0 | 2265.00 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 187962 | -1.0 | 0.0 | 2543.22 | 0.0 | 0.0 | -1.0 | 0.0 | 0.0 | -1.0 | 0.0 |

| 188113 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

516 rows × 10 columns

版权声明:本文为qq_39215918原创文章,遵循 CC 4.0 BY-SA 版权协议,转载请附上原文出处链接和本声明。